When your credit score is not good enough to receive a loan, you might ask yourself what you can do to raise it, and how to do it quickly. Well, depending on why your credit is too low, you might have a few options. For instance, if you just have some credit card debt and that is what is hurting your score, then you definitely have more options than someone who has default accounts. Overall, there are multiple different ways to go about fixing your credit that can help you get a loan more quickly.

Pay Down Your Credit Card Debt

Your credit utilization ratio is the amount you owe on your card in relation to the limit on your credit card. The lower this ratio is for you, the better your credit will be. FICO even states that consumers with the best scores use an average of 7 percent of their credit limits. So, paying off all or at least most of your credit card debt could significantly raise your score, and quickly too.

If you don’t have enough cash to simply pay it all off, though, you could also try transferring the debt to an installment loan or a home-equity line of credit. These types of credit do not affect your utilization ratio, and thus do not hurt your score as much. In fact, increasing the number of different types of credit you manage could even improve your score as well. It is also important to note that you should keep your credit card account open even when you are done using it. This is because, once the account is closed, that card is no longer factored into your utilization ratio, so debt on other cards would be even more harmful to your score than if the other account was still open.

Pay Your Credit Card Bill by the Statement Closing Date

Credit card issuers often report your current credit card balance on your statement due date and not the payment due date. This means that if you are paying your balance right before the payment due date, then you might not be paying it early enough to help your credit score. If you make your payment before the statement closing date, however, then your low or zero balance will show up on your credit report This date can be found directly on the statement.

Ask for a Credit Limit Raise

Most of the time, credit issuers are willing to raise your credit limit yearly. By having a higher limit without using more credit, your credit utilization ratio will improve. This will help increase your credit score. But, if a large increase is granted, your credit report may get pulled. If this happens, then you receive a hard inquiry on your report which can inevitably hurt your score.

Piggyback Off of Somebody Else’s Credit

This strategy is often used for young people with little credit history. So, a parent could add their child as a user on their credit card and then that account history would show up on the child’s credit report. This of course depends on the issuer reporting it, but they do most of the time. If the parent had great credit history, then adding their child to their credit card account could immediately impact their child’s credit in a positive way. You don’t have to be related to someone to be added to their credit card account, though. Most of the time, credit card companies will permit anybody to be added to the cardholder’s account.

Take the Negative Information Off of Your Credit Report

It is imperative that you check your credit report in order to understand what is affecting your credit score and how. You can check your credit report for free once a year from all three major agencies (Experian, TransUnion, and Equifax) at annualcreditreport.com. Removing the information that hurts your score can significantly raise your score, especially if what is hurting your score occurred within the last two years. You need to make sure none of the negative activity is fraudulent. If somebody attempted to steal your identity, then your credit could be hurt in exceptional ways. You also have to make sure no lender has reported something mistakenly. If either of these things occur, you need to take steps to remove this information immediately, either by blocking the fraudulent activity or contacting the lender who made the mistake.

You can also fight to get mistakes removed from your record. If your payment history is otherwise spotless, yet you make a mistake and accidentally make one late payment, then you can contact the biller and ask them to remove the delinquency from your account. Taking information like this off of your report could greatly help your credit score increase.

Be Patient!

If you need a loan quickly, this option might not be the best for you, but being patient can go a long way. If you continue building a strong financial history, overtime, your credit score will go up. The further away you get from a delinquency on your credit report, the less that delinquency impacts your score. The length of your credit history actually makes up 15 percent of your credit score, so just letting time pass while acting responsibly in terms of your credit, will raise your score.

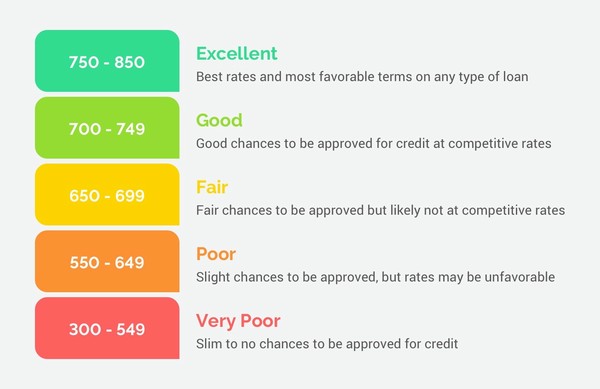

Consumers with the highest scores, typically above 800, have an average account age of at least 11 years, with their oldest account being opened 25 years prior. This means that the longer you exemplify good credit behavior, the better your score will be. Closing your cards will not hurt you score in this area because the behavior from that card will still show up on your credit report and factor into the age of your credit history for at least ten more years. Opening a new card does lower the average act of your accounts, though. So, letting time pass can greatly boost your credit score if you exemplify continuous financial responsibility