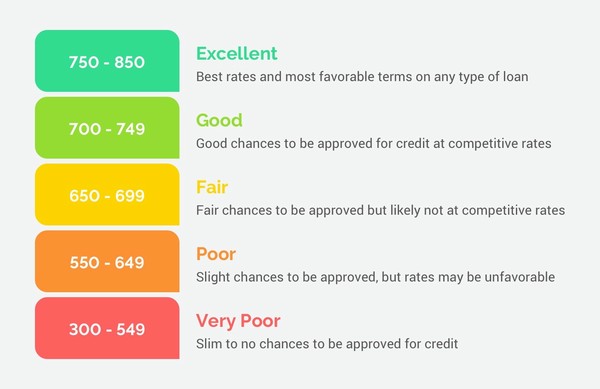

FICO scores were created in order to help lenders make faster, more efficient decisions when it comes to determining a consumer’s risk. Understanding how FICO scores work may seem difficult at first, but there are a couple of factors that end up determining the score you are given. If your number is higher on the 300-850 scale, then you are considered a less risky consumer. Typically, a score above the mid 700s is ideal for a lender.

If your credit score did not exist, then lenders would have to pull your credit report and spend hours looking it over to decide your lending risk. With a credit score, lenders can essentially see an accurate depiction of what is in your report by just analyzing a single number. To create that number, companies like FICO take the financial information from your credit score and use a mathematical model to forecast your lending risk. There are many factors that go into this model.

Payment History

Your payment history makes up 35 percent of your credit score because it is so important. This is because the lender would expect you to continue the same payment habits you have exemplified in the past, preferably over many years. If you do not have a long payment history, then you are more likely to be judged by a single mistake.

If multiple years ago you accidentally paid a bill late, but your payment history has been of high quality since, then a lender most likely would not penalize you for that mistake. But, if you made a mistake more recently, then a lender would have to question what might have changed in your life to cause that mistake, and if it is possible that this mistake could turn into a trend. So, even one missed payment can drop your score for that reason, and if you pay late habitually, then your credit score would drop even lower and you would be considered extremely risky.

Credit Utilization

Your credit utilization ratio is the amount you owe in comparison to the total line of credit you have borrowed. This ratio accounts for 30 percent of your FICO score. This means that if you were to charge a lot of money every month, but also pay your balance completely, then your ratio would indicate that you are not a risky borrower as that information would show up on your credit report. But if you were to max out all of your credit cards, then your credit utilization rate would be much worse. Even if you made each payment on time, it would not be too difficult for a lender to worry about your ability to take on another line of credit and make those payments on top of your current payments. So, high debts can cause your FICO score to be lower.

The Length of Your Credit History

Making up 15 percent of your FICO score, the length of your credit history is also important. The longer your credit history, the more a lender can predict about your future behavior. So, if you have a payment history consisting of many years of on time payments and low debt, then a lender could assume that this good behavior will continue. On the other hand, if your credit history is short, meaning you just began building it, then lenders could be skeptical about your risk as a borrower. They cannot make a reliable decision without enough history to support that decision. The good news is that it often only takes one or two years of healthy credit use for lenders to begin trusting you.

The Types of Credit You Use

If you have proven that you can make payments on not only one type of credit loan, but many, then you will be considered more trustworthy to lenders. For example, if you responsibly handle all of your credit cards, student loan debt, mortgage, and car loans, then you have proven that you can most likely handle multiple lines of credit at once. This category is not as important as some of the others when determining your FICO score, but it still does effect it by 10 percent.

Inquiries

The more you ask for loans, the lower your score can drop. Even if you have a trustworthy history of paying your credit debt off, asking for loans often will still hurt you. Lenders see this as concerning because they assume something is wrong in your life and that it is what is causing you to need more money so often. While this may not be true, it is enough to deter lenders from loaning you money. Lenders can see how often you ask for credit because each time you do, the bank or lender notifies the credit reporting agencies and a hard inquiry gets put on your credit report. This category also makes up 10 percent of your FICO score, which, again is not a huge portion of your score, but it is enough to raise concern if something is wrong.